The COVID-19 pandemic was the biggest disruption to the movement of human beings ever. At no other time in history have so many people stopped moving at the same time. Five years later, the profound effects of that mobility shock are still playing out in every country on Earth, including Australia.

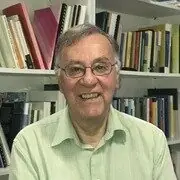

Although it’s hard to confirm whether migration is back to ‘normal’, let’s say we expected migration to follow the trend it was on in the six years prior to the pandemic. If you compare our migration numbers to that trend (see Figure 1), by December 2024 we were fast approaching the level we expected to be at.

But the story doesn’t end there. Net overseas migration (NOM) is now falling rapidly. Why? What are the economic implications? And after a period of huge volatility, how can we achieve a ‘soft landing’ in migration terms?

Why is NOM plummeting?

Net overseas migration is the difference between long-term arrivals and departures. Before the COVID-19 pandemic, NOM was growing at a comparatively steady rate.

But when the pandemic hit and borders closed, NOM plummeted into negative territory. During the lockdowns, we had a cumulative NOM shortfall of more than 500,000 people. And then when borders reopened, NOM surged again.

This was entirely predictable because migration is a function of demand. That demand didn’t disappear during the pandemic – it was just bottled up. As soon as borders reopened, universities, farms, and other businesses desperately needed more migrants to stay in business. So, there was a big surge in NOM to meet the pent-up demand (see Figure 1).

But that surge is now well and truly over and NOM is dropping like a stone. Why is that? To understand any movement in NOM, we need to look at long term arrivals and departures separately.

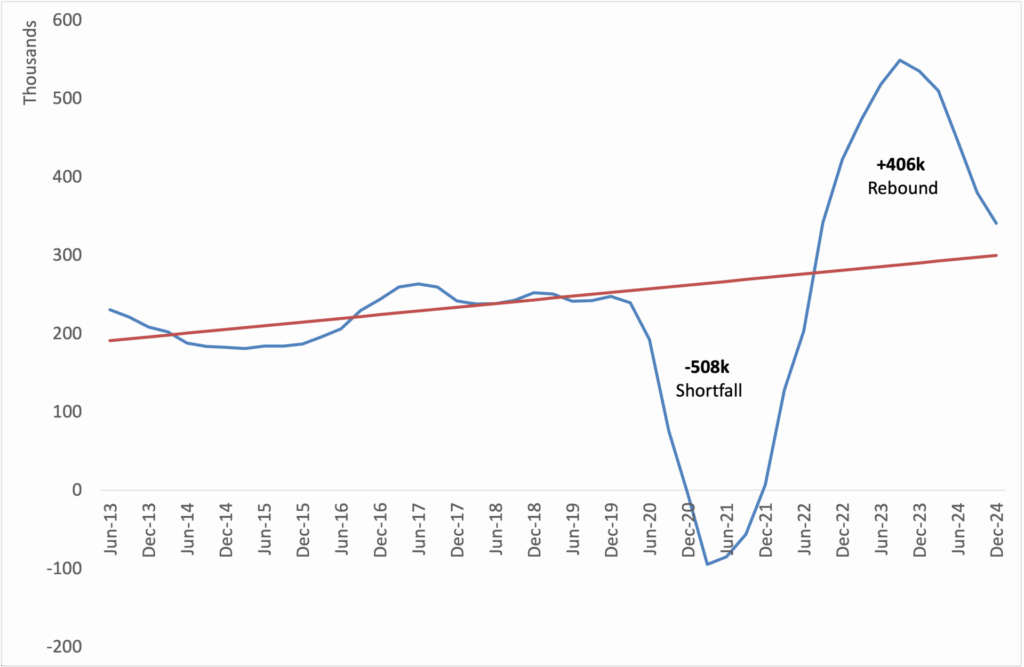

In the five-year period since the pandemic first hit, Australia has had a massive cumulative shortfall of migrant arrivals. Because of COVID-19, we received 636,000 fewer migrant arrivals than expected based on the pre-pandemic trend (see orange line in Figure 2).

There was a huge drop during the pandemic, then a bit of a catch up afterwards, but now arrivals are falling again. This is partly due to government policy, including cutting international student arrivals, which is aimed at addressing concerns about the large NOM surge. There was a small post-pandemic arrivals bump for the 18 months between December 2022 and June 2024, but it was never anywhere near enough to make up for the colossal shortfall in arrivals caused by lockdowns. Compared with the pre-pandemic trend, cumulative arrivals have been very low over the past five years.

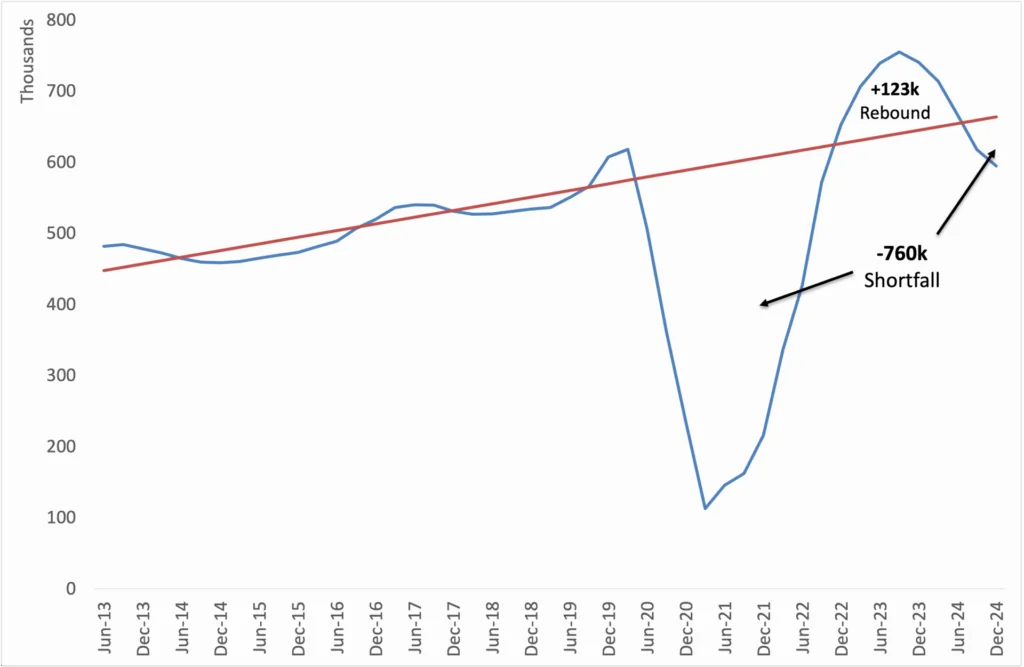

But if cumulative arrivals are so low, why did we have such a big surge in NOM? Answer: departures. When lockdowns happened, it wasn’t just arrivals that stopped – it was departures too, as shown in Figure 3. Other countries stopping arrivals meant that we had to stop departures. And out of compassion for stranded temporary migrants – and the Australian businesses dependent upon them – many visa extensions were provided. Most of these will expire in the next few years. Relative to trend lines, it’s the combination of a small arrivals rebound (in Figure 2) and the large, delayed departures bulge (in Figure 3) that led to a big surge in NOM.

So why did this surge come to an end, and why is NOM now dropping so quickly? It’s because we’re over the post-pandemic arrivals bump – partly due to policy cuts – and the departures bulge is working its way through the system. As Figure 3 shows, there has been an uptick in departures over the most recent 18 months of data (from September 2023 to December 2024). Lower arrivals plus higher departures equals lower NOM.

Which migration flows have shrunk the most?

From 2023 to 2024, NOM to Australia fell by 189,870. The breakdown of this very large decline is shown in the following two tables. The first shows movements (arrivals or departures by visa type) that contributed to lowering NOM between 2023 and 2024, and the second shows movements that contributed to an increase in NOM during that same period.

With 103,700 fewer arrivals and 17,350 additional departures, international Students were by far the largest contributors to the lowering of NOM between 2023 and 2024. Student arrivals included 53,880 in the higher education sector, 23,750 in the VET sector, and 24,120 in the ELICOS sector. Student departures also increased

substantially as did departures of those on Working Holiday visas. Arrivals of Temporary Skilled workers were down by 3,600 and their departures up by 2,840, a net loss of 6,400.

Finally, people who stayed in Australia on a Visitor visa long enough to be counted into the population made up the second-largest group contributing to the lower level of NOM. These are people who arrived in the country on a three-month Visitor visa and then converted onshore to another visa that allowed them to stay longer. The capacity to hop onshore from a Visitor visa to a Student visa was stopped by the federal government in 2023, and this likely explains the decline in those on Visitor visas being counted into the population. The other substantial category that may have declined is people arriving on a Visitor visa and then claiming asylum.

Table 1: Movements contributing to lowering of net overseas migration (NOM) from 2023 to 2024

| Movement | Number |

| Student arrivals | -103,700 |

| Temporary Visitor arrivals | -31,320 |

| Temporary Other arrivals | -18,380 |

| Student departures | -17,350 |

| Working Holiday departures | -13,150 |

| Temporary Other departures | -10,270 |

| Bridging departures | -3,860 |

| Temporary Skilled arrivals | -3,600 |

| Temporary Skilled departures | -2,840 |

| Permanent Other arrivals | -1,430 |

| Temporary Visitor departures | -1,390 |

| Working Holiday arrivals | -930 |

| Permanent Skilled departures | -510 |

| NZ Citizen departures | -110 |

| Permanent Humanitarian departures | -40 |

| TOTAL movements contributing to lowering of NOM | -208,880 |

The movements contributing to an increase in NOM between 2023 and 2024 were relatively small and all except one – the small category of persons arriving on Bridging visas – were part of either the permanent migration program or were Australian or New Zealand citizens. With an additional 2,900 arrivals and 2,160 fewer departures, the movement of Australian citizens played the largest role in increasing NOM between 2023 and 2024.

Table 2: Movements contributing to increase in net overseas migration (NOM) from 2023 to 2024.

| Movement | Number |

| NZ Citizen arrivals | 4,430 |

| Permanent Skilled arrivals | 3,920 |

| Permanent Family arrivals | 2,440 |

| Australian Citizen arrivals | 2,900 |

| Australian Citizen departures | 2,160 |

| Permanent Humanitarian arrivals | 1,290 |

| Permanent Other departures | 970 |

| Permanent Family departures | 660 |

| Bridging arrivals | 230 |

| Permanent Special Eligibility arrivals | 10 |

| TOTAL movements contributing to increase of NOM | 19,010 |

What does this mean for Australia?

The economic implications of the drop in NOM are significant. It’s unlikely this decline will slow down right away. The cycle of policy cuts to migration that began in the 2024 election season is still working its way through the legislative and policy process, and is likely to place downward pressure on arrivals for some time. Meanwhile, the extensions to temporary visas granted during the pandemic are expiring. So, if we’re not careful, we might be back in ‘pandemic world’ in a couple of years, worrying desperately about how we’ll fill skills and labour shortages.

From the perspective of the Australian economy and society, the best-case scenario is a steady net inflow of overseas migration. Australia depends on immigration to offset the ageing of its population and to meet labour demand. Population ageing happens when the number of elderly people grows relative to the number of working-aged people supporting them. That can lead to a situation known as a ‘demographic winter’, when youth becomes a scarce resource, and the population and economy of a country shrinks and stagnates, leading to lower standards of living for everyone. Australia imports working-aged people to offset this problem, and that has helped make Australia one of the richest nations in the world.

The problems start when migration happens in sudden, destabilising bursts and troughs rather than through a steady stream. By disrupting all forms of human mobility, the pandemic completely destabilised the migration systems of Australia and many countries, and we are still recovering from that shock.

The way to steady the ship is not by making sudden movements. Re-balancing migration will happen naturally as regulated supply meets Australian demand in the coming months and years. Sudden radical slashing or opening of new migration streams will just contribute to prolonging the volatility.

That said, the current rapid rate of decline in NOM presents a risk of a ‘hard landing’, where we undershoot the levels of migration required to keep the Australian economy running smoothly, as we did during the pandemic.

If the aim is a soft landing from the recent NOM highs, there may be arguments in favour of reviewing some of the proposed or actual restrictions introduced in the past 18 months – especially those that may have been election-season reactions to the perceived risk of a prolonged NOM blowout that has not eventuated.

This is not the same thing as an argument in favour of higher migration levels forever. On the contrary, the wider aim should be an orderly post-pandemic return to stable, normal levels of migration – whether that is the pre-pandemic normal, or a ‘new normal’ decided through proper consultation and deliberation.